One in three wealth managers reduce exposure to US in Q1 of this year, according to the ARC Market Sentiment Survey, a quarterly poll of 78 investment management CIOs examining the 12-month outlook for the major asset classes and sectors.

The survey reveals a cautious tone, with conviction levels declining across all major asset classes – particularly with the US, it said in a statement on 2 April.

The geopolitical and macroeconomic backdrop shaped by the early months of President Trump’s return has led many firms to reassess exposure to US assets. Sentiment was 4% net negative to US assets compared to 36% net positive a year ago. While the net sentiment towards equities overall remained positive at 29% this has also softened from 40 per cent in Q1 last year. Bonds suffered the biggest drop in sentiment; it was down to 29% from 44% net positive a year ago.

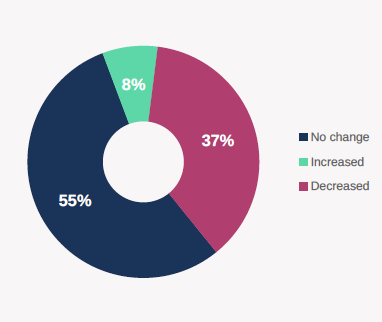

The investment consultancy highlights that while many investment firms made no changes, those that did primarily reduced US equity exposure, particularly in large caps and technology stocks.

Some increased exposure to US small and mid-caps, while some used call options on the S&P 500, suggesting a targeted rather than broad bullish outlook. Firms reducing their exposure actively hedged USD exposure and reduced equity allocations, reflecting a defensive strategy amid market uncertainty.

See pie chart below for US exposure changes:

Dr James Cooke, deputy CIO at ARC, says: “This is the biggest negative sentiment quarter-on-quarter US swing we have seen since our Market Sentiment survey began in 2010. President Trump’s ‘Liberation Day’ tariffs threaten to damage sentiment further. Higher asset price volatility ought to provide opportunities for active managers to demonstrate the value they can provide. Those managers not making changes indicate they intend to look through the Trump-induced volatility believing tariff imposition may be temporary.”