Ritu Vohora (pictured), capital markets specialist at T. Rowe Price, dives into US equities.

Given the unprecedented nature of the coronavirus pandemic, the strong recovery in US economic growth during 2021 has been remarkable. The US equity market has similarly rallied sharply, surpassing previous peak levels in just a few quarters, with some companies posting close to best‑ever earnings results in early 2021.

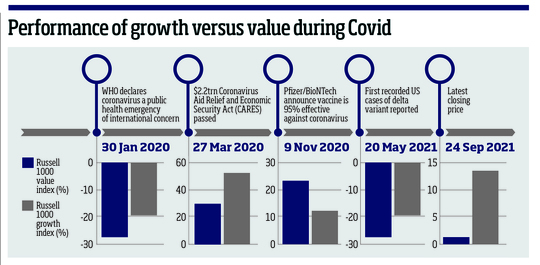

One of the dominant market themes to emerge in late 2020 and continue into early 2021 was the sharp swing toward value companies at the expense of more richly priced growth‑oriented stocks. More recently, however, the strong impetus behind value companies has moderated, with some suggesting the ‘great value stock rotation' is over already. This view could be premature.

The continuing economic rebound is reason for optimism. US consumers are in good shape with a large pool of excess savings ready to be deployed; business inventories are lean, which is likely to lead to a capex pickup; the government is set to roll out significant fiscal stimulus; and the US Federal Reserve appears comfortable keeping monetary policy accommodative.

Looking forward, we are expecting continued fundamental improvement for many companies. We are also anticipating a progressive rotation within the value landscape, with investors gradually shifting focus from early‑cycle and deep‑value companies towards higher‑quality value stocks as the next beneficiaries of the economic cycle.

The respective performance of value and growth‑orientated sectors during different stages of the cycle is likely to be a key consideration over the coming year and beyond. Broadly speaking, the principal difference between the two areas is the large allocation toward technology for growth investors, versus a similarly significant allocation to financials for value. To the extent technology stocks outperform, most likely, growth investors will outperform, while the opposite is generally true if financials outperform. Historically, value‑orientated areas have tended to perform best in the earlier stages of economic recovery and during periods of higher inflation and/or rising bond yields.

While innovation is a concept more often associated with growth companies, it is important to try and understand the secular change occurring across the market. We are continually looking for opportunities to invest in innovative, potentially disruptive companies at attractive valuation points - for example, if the company has fallen out of favour with investors due to some short‑term issue or challenge.

Microsoft is a good example of a business that many value investors were not willing to consider, but should have.

The company fell out of favour with investors as both the range and quality of its products were seen as lagging major competitors such as Apple and Alphabet.

However since then it has invested heavily in upgrading the range and quality of its product set, entered into strategic partnerships to expand the market for those products, and entered new, high‑growth business areas, such as cloud systems and services.

Powerful secular forces can also create opportunities for value‑oriented investors in mature industries where the market may not fully appreciate the extent of the tailwind. For example, over the next three-to-five years, the growth related to online shopping could provide a meaningful tailwind for companies that produce the containerboard used to package products for shipping. We also like the dominant players in the US air freight and logistics industry, such as UPS - companies offering exposure to rising e‑commerce shipment volumes, which also have several levers that can expand their gross margins in the coming years.

While we saw a very strong, value‑led, US equity market from Q3 2020 through to the end of Q1 2021, sentiment toward value companies appears to have shifted again, with some of the stronger-performing value areas giving up earlier‑year gains.

A resurgence in coronavirus cases in recent months has raised concerns about the nascent US economic recovery and undermined confidence in the value stocks most directly impacted. This has seen a lot of the early‑year investment flows into value companies reversed in recent months. However, it is worth noting, within the value landscape, we are seeing early signs of the expected rotation, with investors moving out of cheaper, economically sensitive value areas and reallocating toward higher‑quality value companies instead. Going forward, we anticipate company quality being a more influential factor in driving the returns of US companies. However, with elevated multiples across much of the market, it is prudent to remain mindful of valuations.

Ritu Vohora is capital markets specialist at T. Rowe Price