Index funds and ETFs have experienced very successful decades recently. Their assets under management rose sharply and their actively managed, traditional competitors were often falling short, performance wise, says Jiří Šindelář, investment analyst, former FECIF deputy chairman, now working at Czech based MONECO investment company.

But the commentary success of passive investments was frequently met with scepticism, with voices being heard on how ETFs will erode market efficiency and cause abnormal volatility and liquidity issues. Were these concerns justified?

A new study focusing on the US large cap equity market found interesting results.

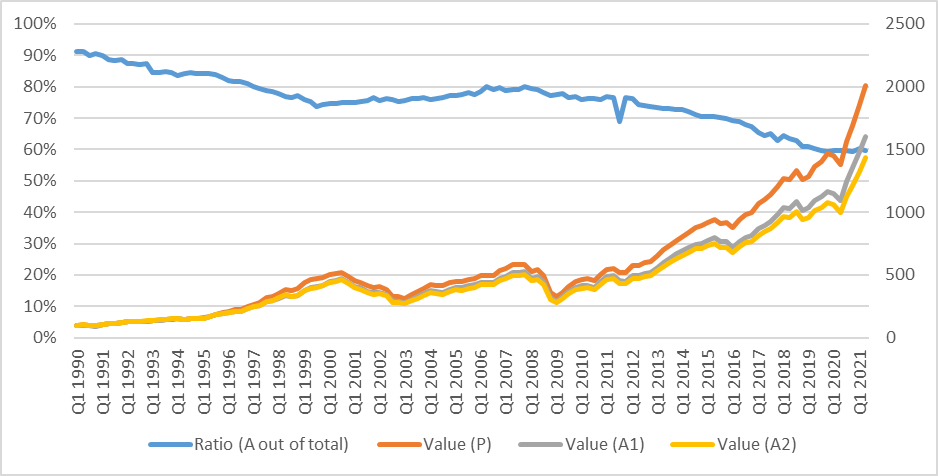

One can hardly imagine more premier investment parquet than US blue chip stocks. It is also a market where ETFs and other index investments gained a strong foothold. Our study, composed of analysis of some 2,173 managed investments over the period 1990-2021, shows that index vehicles´ market share rose from a humble 8.7% in the early 1990s to almost 41% at the beginning of 2021.

While still not composing a majority in the market, assets wise, such growth in size is very strong. Mind you, we have surveyed not only typical mutual funds, but all managed investments - insurance funds, trusts, individual portfolios, closed-end funds and so on.

What results did both active and passive investments achieve in terms of performance?

Not surprisingly, passive (index) investments achieved significantly higher returns after fees, confirming the long-term observations of many professionals. The more unexpected result came afterwards: the active managers, while bringing up lower returns, have achieved those with significantly reduced volatility.

This is a new thing and it suggests that even "old school" active investments might provide notable benefits in a combined portfolio. The graph summarizes those outcomes on a simulated investment of 100 USD on the first day of 1990, going through average passive investment (P) and two active strategies blend only (A1) and blend, growth and value combined (A2).

The key question remains, though. Has the rising share of passive investments impeded market pricing efficiency? We particularly examined a scenario where index investing's near dominance would create inconsistencies, under or over-priced stocks that could be exploited by active managers.

Yet no significant link was found in this regard, both in terms of investment returns as well as their volatility. In other words, we did not find evidence of passive investing eroding market efficiency - so far. While this cannot serve as a definitive judgment, as the ratio of index vehicles is strengthening further, it indicates an important hallmark.

Investors and advisers alike should be not ashamed of ETFs and other passive vehicles, they do not seem to instil some kind of apocalypse on the market, as envisaged by some active managers. These too, however, have found their purpose in the data, with reduced volatility over their passive counterparts. In other words, a combination of both approaches in individual portfolios seems to be viable, enriching the "good old" diversification paradigm with a new passive-active axis.

More experience on this will be gained over time, as passive investing popularity is skyrocketing. And our data confirms, there is a reason - although active investments still have a chance to bounce back with a new purpose.

By Jiří Šindelář, investment analyst, former FECIF deputy chairman, now working at Czech based MONECO investment company.

Sign up to our Newsletter

Unlimited access to real-time news, industry insights and market intelligence

Latest Stories

Sign up to our newsletter

Unlimited access to real-time news, industry insights and market intelligence.

© Investment International | Site By Furness Media