Take a look at stock market concentration in emerging markets and assessed portfolio construction implications for investors, says Lena Tsymbaluk, associate director of manager research at Morningstar.

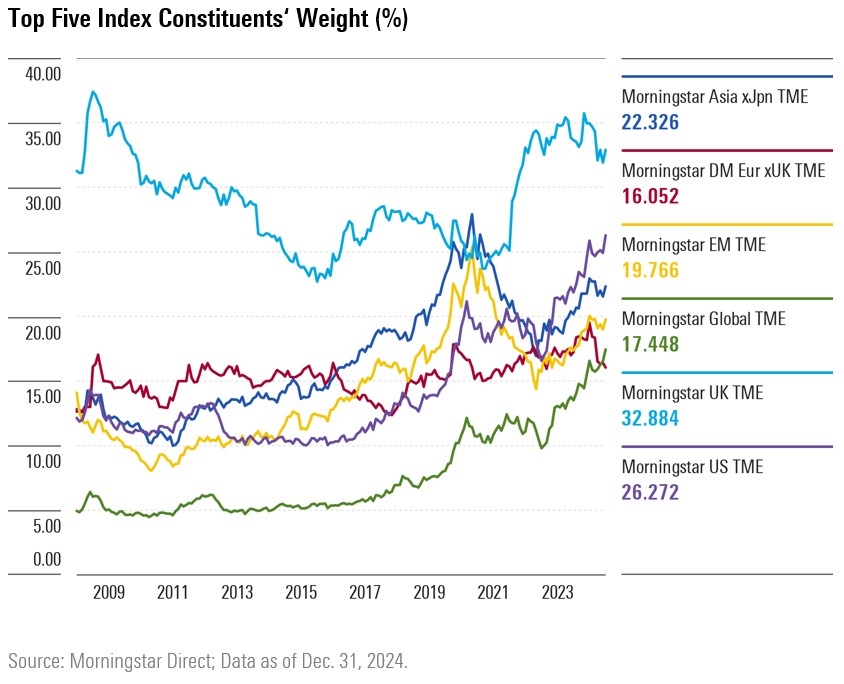

The rise in market concentration in the US equity market has been a significant trend in recent years. The top five names in the Morningstar US Target Market Exposure Index—all mega-cap technology companies that are part of the “Magnificent Seven”—almost tripled to 32.6% as of December 2024 from 11.0% a decade ago. Their dominance in sectors such as artificial intelligence, cloud computing, e-commerce, and semiconductors has been the primary driver of growth.

Much like the US market, the technology sector has become a dominant force in emerging markets, driving a significant portion of the market’s growth. Companies like Alibaba, Tencent, Samsung Electronics, and TSMC have become major drivers of market capitalisation. At its peak in late 2020, concentration in the top five index names accounted for as much as 25% of the Morningstar Emerging Markets TME Index, similar to the levels observed in the US market.

Similarly, country-level concentration is notable, with the top five countries—China, India, Taiwan, Korea, and Brazil—accounting for 80% of the Morningstar Emerging Markets TME Index.

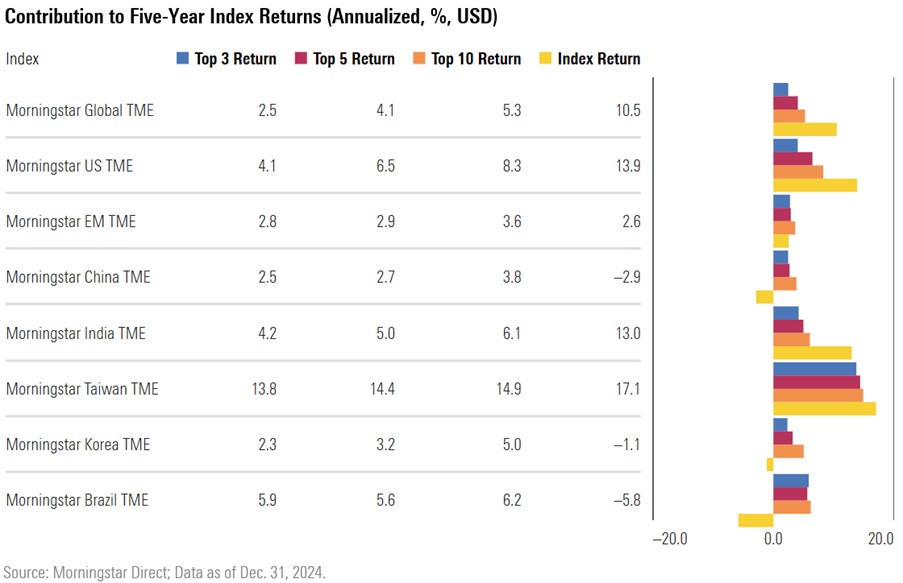

Contribution to index returns by the top names

The leading index names are frequently major factors in influencing the overall market performance.

In the broad emerging-markets space, the two largest names in the Morningstar Emerging Markets Target Market Exposure Index, TSMC and Tencent, drove 50% of the benchmark’s returns over the past five years (to Dec. 31, 2024).

In Taiwan, Korea, and Brazil, where market concentration is notably high, the top five companies have been responsible for most of the market returns.

In contrast, the market rally in India over the past five years has been much more broad-based. The top five companies in the index were responsible for about 38% of the market returns, as overall growth was largely driven by smaller companies.

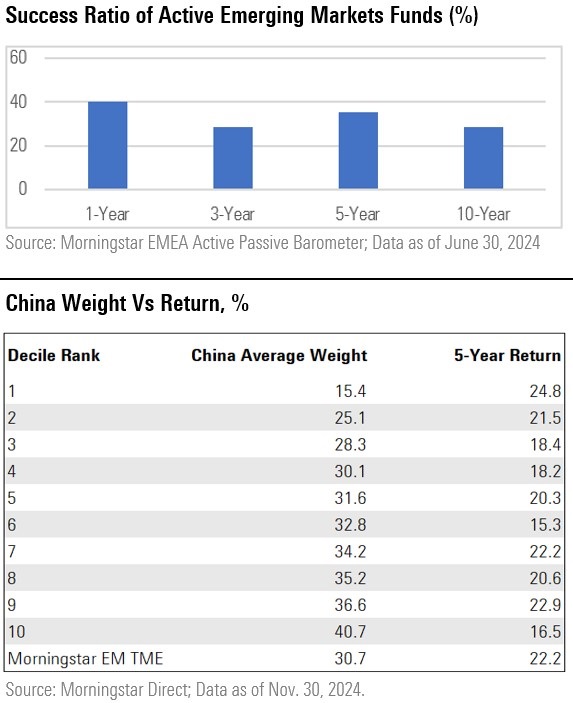

Success ratio of active funds – emerging markets

Morningstar’s Active/Passive Barometer shows that in the emerging-markets category, only 35% of active funds have managed to beat their passive peers over five rolling years to end June 2024. This was partly driven by the two top names in the Morningstar Emerging Markets TME Index, TSMC and Tencent, which drove 50% of the benchmark’s returns in the period. Underexposure to these two names proved a common source of underperformance for many active managers.

The one-year success rate was slightly better at 40%. One of the reasons was a bearish view of China adopted by many active emerging-markets managers, which proved to be beneficial considering China’s economic slowdown and regulatory challenges. By reducing their China exposure, active managers had the flexibility to have higher exposure in stronger performing markets, such as India and Taiwan.

As shown in the table below, the top 10% of the funds in the Morningstar Global Emerging Markets Equity peer group with the lowest China weight—averaging 15%— had the strongest five-year return (to Nov. 30, 2024).

In addition, some of the top index names, such as Alibaba and Samsung Electronics, widely held by passive funds, detracted from performance over the period.

Finally, skilful active managers in emerging markets added value by investing in niche markets or off-benchmark stocks with strong performance, such as MercadoLibre (Argentina), Kaspi.kz (Kazakhstan), and Nu Holdings (Brazil).

What Should Investors Do About Concentration?

It can be challenging for active managers to beat market indexes and, therefore, passive funds, when giant-cap stocks make outsized gains, as tends to be the case in periods of high concentration. This is because the biggest driver of returns tends to be relative weight in the top stocks as opposed to stock selection elsewhere.

This has been the case for US equities, with the “Magnificent Seven” playing a major role behind the market rally in recent years. The US market is also arguably the most efficient and competitive globally. The case for passives is overwhelming—only 8% of surviving active funds in the US large-cap blend category beat the passive alternative over the decade ending June 2024.

In emerging markets, highly concentrated country-specific active funds, such as those focused on Taiwan, Korea, or Brazil, may struggle to outperform passive alternatives when returns are driven by a few dominant index stocks. However, investors opting for passive strategies in markets where high concentration is the norm should be mindful of the significant downside risk they face if market conditions change. Passive funds lack the flexibility to adjust to shifting market dynamics, leaving investors vulnerable during downturns or when the top stocks underperform.

Active funds have a place in markets that are less concentrated or where investment opportunities are more abundant owing to market inefficiencies. Active funds can also prove useful for investors who wish to gain exposure to specific segments of the market, such as growth or value stocks, or small- and mid-cap companies, many of which, particularly in the case of emerging markets, do not make it onto indexes.

The Chinese and Indian stock markets are fertile grounds for active managers, given their relatively lower concentration than other emerging markets, and local retail investors have occasionally spurred large momentum- or sentiment-driven market swings.

Investors can tilt the odds in their favour by focusing on high-quality active funds, which are managed by experienced and skilled investment teams based on time-tested and consistently applied approaches. A long-term view is also essential to investment success, and investors can be best served by staying the course.

By Lena Tsymbaluk, associate director of manager research at Morningstar