There’s no doubt about it – India has caught the stock market bug. Rather than piling into the nation’s largest names, however, domestic investors have made it clear they are far more interested in the smaller end of the market, say Abhinav Mehra and Andrew Draycott, co-managers of the Chikara Indian subcontinent Fund.

Heavy inflows have sent the Nifty small cap 250 index 71% higher over the past year, while the Nifty mid cap 100 index rose by 64%. In comparison, the benchmark Nifty index advanced by 28% over the same period.

The performance is no doubt impressive. But with valuations now reaching unsustainable levels, we feel it is time for investors to look at the alternative opportunities offered by India’s large-cap stocks.

Correction risk

Strong domestic sentiment towards Indian small and mid-caps has existed for a few years now. But as the graph below shows, it has picked up particularly since mid-2023 in response to strong performance and the growing certainty of a BJP victory in this year’s general election.

In the first 10 months of this fiscal year alone, it is thought that inflows to Indian small-cap funds have increased by 92% on the entire previous 12-month period.

Source: AMFI, Kotak Institutional Equities

This level of growth, however, is unlikely to be sustainable.

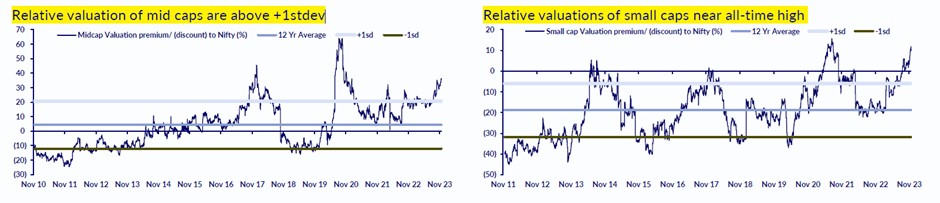

Figures below from capital markets group CLSA below show that the relative valuations of small-cap stocks in India is near all-time highs. Mid caps, likewise, look stretched.

Source: CLSA

The worry is, the high price to equity ratios at which these companies are trading is not always justified by their underlying strength and outlook. As Indian investment bank Kotak put it recently: “The general euphoria on the street has resulted in a dangerous obsession with superficial narratives at the expense of fundamentals and numbers.”

In other words, small and mid-cap stocks are arguably overvalued, increasing the risk of a market correction.

And just as their smaller size can lead their market capitalisation to rise by a greater percentage on the way up relative to their large-cap peers, it can also lead them to suffer more on the way down.

As the below chart demonstrates, the smaller the company, the longer the recovery period tends to last after a mass drawdown in India.

Large-cap opportunity

We’re not saying there will be a correction imminently. In fact, the sheer strength of domestic sentiment towards small- and mid-cap stocks is likely to be hard to shake.

But that’s not to say it will not happen.

Were there to be some large unforeseen global or domestic event, we could very much see the focus shift back onto fundamentals. This possibility is already causing some concern amongst some institutions.

India’s market regulator, SEBI, has asked the nation’s asset managers to give investors more information about the risks associated with small and mid-cap funds. It is also reported to be reviewing stress tests to see what impact large outflows could have on the value of these products .

But where these concerns centre around whether any “gas is in the tank” for India’s small- and mid-cap stocks, the focus should instead be on how much still remains for its large-caps.

A robust rise in underlying earnings among these companies is being significantly undervalued.

As the below chart from Motilal Oswal shows, overall return on equity is greater in the Nifty 100 than anywhere else in the market. However, its overall trailing PE ratio is significantly lower.

This disconnect is particularly apparent in private banking.

Despite these firms consolidating market share for some time now and benefiting from general banking demand growth across India, valuations have actually compressed over the last few years.

Take HDFC and Kotak Mahindra Bank, for example. Both sit around their lowest valuations since the global financial crisis despite posting consistently strong financial results.

Time for a new approach?

Relative valuations give large-cap Indian stocks greater room for outperformance than small and mid-cap stocks right now while offering more insulation against the risk of a correction.

That’s why they should be moving up the priority list for investors in the country.

If we see an increase in foreign investment flows into India (as expected this year if US interest rates ease and the dollar weakens), then large-cap Indian stocks could receive just the momentum they need for a positive rerating.

By Abhinav Mehra and Andrew Draycott, co-managers of the Chikara Indian subcontinent Fund